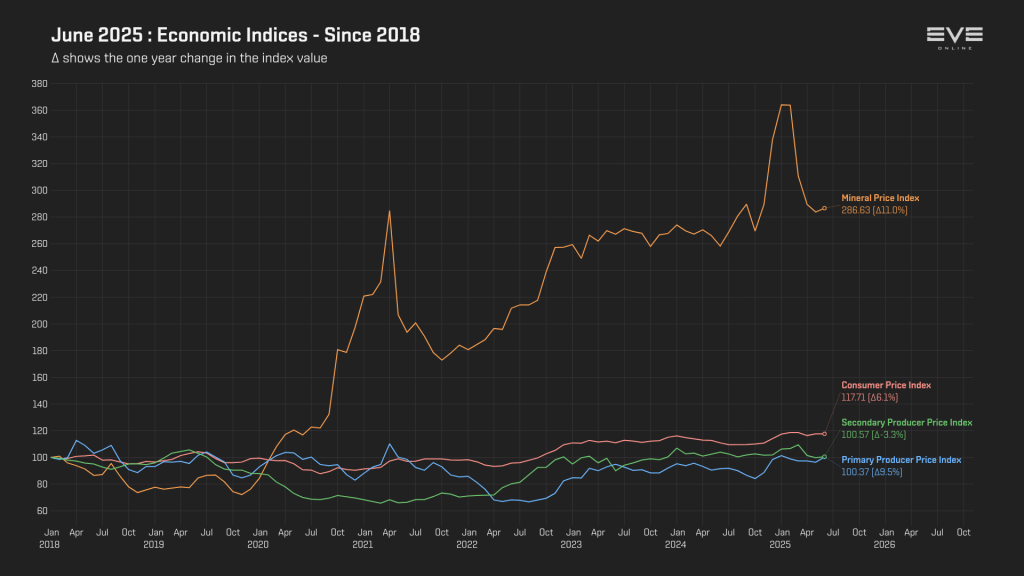

Pyerite seems to be the consistent story from week to week this month, and the elephant in the room when online with my corp. In the past couple of months, I have been considering creating a mineral index because of its centralness to industry, and because for the past two weeks, all I have thought about is pyerite, industry, and markets, leaving less time for other things to enjoy.

In the resulting discussions from last week’s post on July’s MER, someone chimed in with the fact that other sources of pyerite are going unbuffed by CCP, both R4 moon ore and Gneiss.

The problem with R4 moon mining is unprofitable in comparison to Metenox moon mining, with R4 moons losing their luster as other moon goo becomes more popular with miners, industrialists, and market players. The problem with that is, well, people are leaving pyerite trapped in the moon and not trading in Jita.

Secondly, while low sec enjoys some of the best fights in the game, the mining deposits are a shadow of its High and Null secs brethren, meaning that gneiss is only available for mining in sectors that aren’t conducive to bringing out a big mining fleet. At least with Null Sec, the idea is that the alliances out there are often running their own fleets in the safety of their bloc.

As one can see from these graphs, there isn’t much in the way of gneiss making large profits. While these aren’t demand graphs, clearly the lack of bid activity signals that, at least Iridescent Gneiss, is not in hot demand from buyers.

It is important to note that while the spread percentage of Iridescent Gneiss has skyrocketed in the past month, it may not last. Given that all three types shown here do seem to be on the rise, with the ask price, along with a weakening bid price, the margins seem to suggest that the market has two ways it can go, and it is in a standoff.

Running the volume numbers on Prismatic Gneiss suggests that there is significant demand; however, it is the ask market controls the profit margins. This sets up a price tension that one side is going to have to cave on. Given that the ask volume is trending down, the bid market is clearly meeting the sellers at the ask price, thus boosting the profit margin. Then this drops demand by extension, but also creates a problem with buyers snapping up all the available ore on the market, creating some issues in the long run with supply.

These graphs show CCP is not incentivizing low sec miners to get out to the belts. Given that just regular Gneiss reduces to 2000 units of pyerite, if Gneiss spawn rates were higher, there would be more to effectively reduce down into pyerite, to help the market recover. But there would also be a need to help manage belt security, which CCP will largely leave the miners to the mercy of gankers.

While there is some safety in numbers, mining vessels aren’t all that speedy to warp out and so that could cause more problems. There goes your 1B ISK ship along with all that ore. Mining fleets could ultimately do easy freelance security jobs, getting newbros into low sec and into pvp, but that also could present a mismatch of skill between the gankers outfitted in strong fits and pvp skills and newbros with fits that are going to ultimately be underpowered by lack of pvp skill and experience.

Again, I think at some level that since High Sec mining is the second highest, I do think the high sec buffs are more about helping newbros get into the game and build some ISK wealth so they can ultimately go long term with the game. However, newbros can only do so much mining, especially when the high sec asteroids don’t bring in a lot of pyerite and minerals anyway. Clearly, that is not enough to meet the demand of pyerite and lower the price and sending them out to low sec without proper protection only to get ganked is only dissuading them from continuing.

The sudden influx of pyerite would have the market go haywire, which is probably the reason why CCP is ultimately being highly, and perhaps, overly cautious about pushing moon goo and gneiss too far, but the problem is they still think the price is too high.

The likely story is that most of the pyerite being mined is now being sent through the private contract markets, which is causing the inability to move the price in Jita. At some point, that pyerite does need to come back to the Jita market to affect the price.

Ultimately, the larger problem is CCP looking at the wrong signals on pyerite and ore demand and in order for them to fix the market in the way they see fit they need to be making investments in low sec as a starting point.

Enjoy my analyses? Subscribe below to get my posts directly to your inbox.

No ads. No upsells. Just the content.

Sources

Adam4Eve API – Market Price History

Discord