The Monthly Economic Report for February came out this past week, and while everything was down, I wanted to take the data from previous MERs to see if I could compare market regions to see where there was growth and where there was decline, specifically if the movement in Metropolis I discovered a few weeks ago was cutting into The Forge’s market share.

When comparing just pure raw trade volume, The Forge, of course, dwarfs Metropolis by several times. That is no surprise.

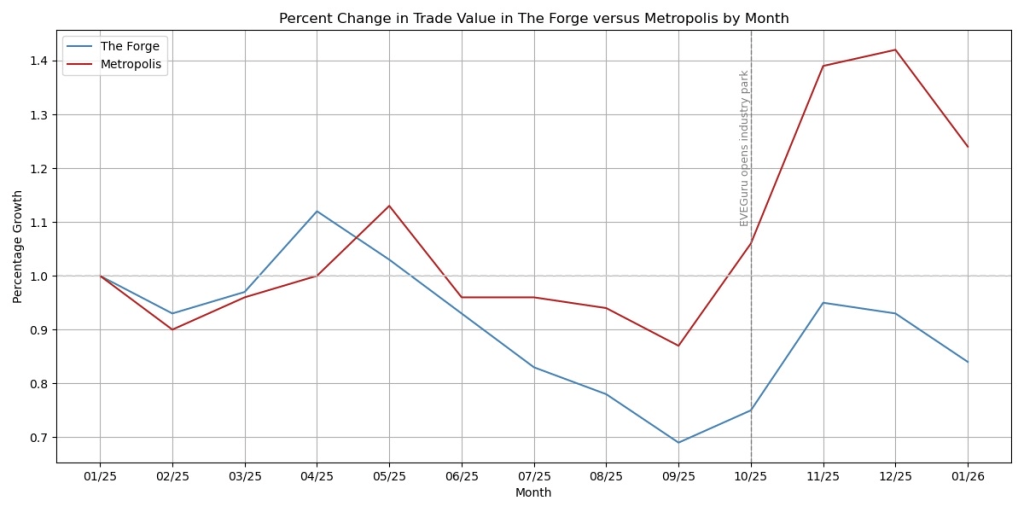

When looking at the log scale, a pattern emerges. Both Jita and Hek follow each other in terms of peaks and valleys. Metropolis is almost always about a month behind. This, too, is unsurprising; after all, they exist in the same universe with the same player base and the same political happenings. But if you look closely at the ends of both graphs, where Metropolis ends higher in 01/26 than in 01/25, The Forge ends lower in the same period.

That signaled to me that there is something going on in those particular markets and led me to this graph below:

In pegging performance to the beginning of 01/25 and its relative position throughout the year, Metropolis’ trade value grows quite significantly over time, whereas The Forge has been slowly declining over the past year in comparison to where it was in 01/2025.

There is something behind this growth from September until peaking in December. The implosion of PanFam in November clearly is what caused the contraction in both markets.

I’ll temper my earlier conclusions that we are seeing Metropolis’ growth from EVEGuru Foundries in Metropolis, because while that is likely helping, Metropolis grew rapidly the month before. So, whatever is elevating Metropolis at that growth rate, EVEGuru Foundries is clearly going to tap into the existing market growth should it continue. This is also to say that while EVEGuru has yet to release production rates using their manufacturing rigs, it is unclear if EVEGuru will affect markets to any degree. It is too early to tell.

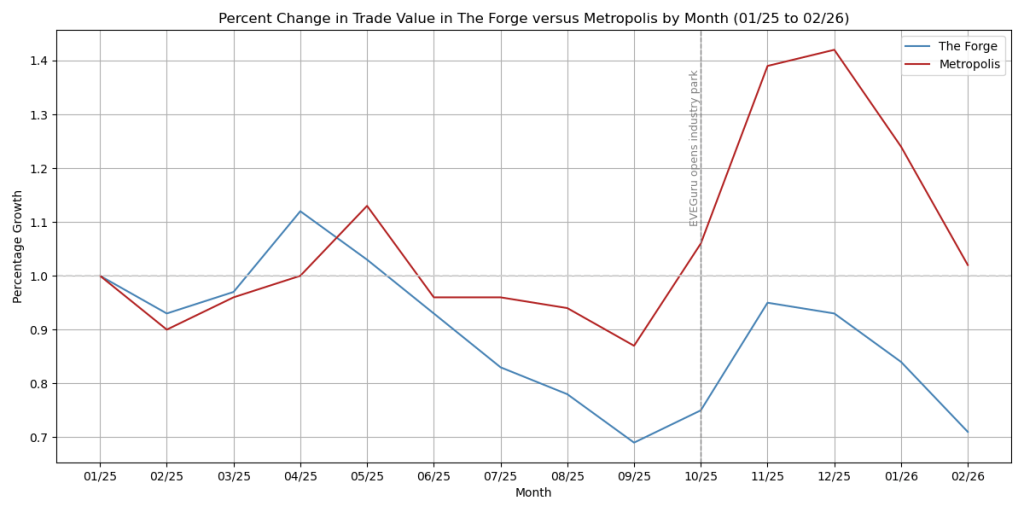

When graphing the trade data with MER February 2026’s data, above, we are seeing that both regions are starting to slide in earnest. If your portfolios are looking a bit rougher than usual, you are not imagining things.

What is going on there is, of course, subject to further exploration in The Forge and the subject of next week’s brief. Is it due to sov null being too quiet (as mentioned above, PanFam’s implosion did burst both markets’ gains), seasonal trends in the user base, or due to timing based on FanFest and expansion plans?

Like the seasons, markets do come back to life eventually, and we’ll see if spring (or lack of) weather in the Northern Hemisphere or FanFest/Expansion help get the markets back in the right direction. Ultimately, with the New Player Experience likely to shake the markets up come later this year, and rumors of changes in market hubs, looking closely at the data seems to be pointing that change is afoot and The Forge/Jita’s dominance is potentially looking threatened.

As always, interested in your thoughts. Write a comment or ask a question below.

If you want to catch my market briefs, like this one, be sure to subscribe to the blog. When a post goes live, you’ll get my post directly into your inbox. Don’t plan on having a regular day to post, so subscribing is the only way you will see everything and stay up-to-date.

No ads, no AI (anymore), no BS.

Sources

Python

Jypter Notebooks

Monthly Economic Reports 01/25-01/26 found on EVE Ref

CrazyKinux revived EVE Online Banter, which was popular among the EVE Online blogosphere when the shift to streaming and video “content” began, and is now calling it: New Eden Banter, so here I am joining the conversation. I am going to stick with economics and data because that is what I cover here, and I don’t want to get too far from the “role play” if I can help it.

Prior to last year, and really for half a minute in 2023, I have been in and out of EVE for a long time. I started playing the game in 2011, fresh out of college, and was seeking something to sink my free time into. I didn’t do much, enjoyed mining, but just mining and selling my ore couldn’t sustain a membership long term. It wasnt until 2023 when I took the Google Data Analytics Career Certificate and other data analysis certificates in Python and R (and joined the right corps) that EVE became sticky for me to a much greater degree. When rejoining last year, I used my programming skills, which led to writing market reports. I actually started writing poetry after leaving because the death glares of r/eve started to turn into anxiety and stress.

But why has EVE stuck around for 23 years? That is the topic for New Eden Banter #1, and I will take a look at my narrow scope of the market and economic reasons why EVE has stayed alive and popular with players, many of them long-term players.

In short, the game’s backbone is based on the player economy. Goons can’t rip apart their opponents without ships, and ships cost money to build (and buy); players just can’t ignore the whims of the market without potentially losing a lot of ISK. To me, the market economy is what cements the level of immersion that is long-lasting.

Market PvP: The 0.01 ISK Wars

There is something really engaging for me when I see a market economy this developed in a virtual world. Coming from Second Life, where the currency is connected to real funds, the idea of a digital, liberal market economy flourishing in a video game is not inherently strange to me. Unlike fantasy MMORPGs where the currency is in gold, silver, and copper, ISK and the marketplace operating like real life currency and the real life stock and commodity markets and that is unique in the sense that because not a lot of games offer such an intense level of a free market simulation and that supply and demand are fundamentally in the hands of the players, but without an IRL economy to keep the market going. You don’t really get that with other games and virtual worlds where real money trading is built in; that space is highly regulated.

CCP has said ISK is not exchangeable for real cash due to the fact that they want the players to effectively have free rein in the economy. If someone wants to scam the money out of another player, CCP is not going to step in and force the scammer to pay the other player back, among any number of illegal money schemes that EVE players perpetrate on the daily. If one wanted to do that with convertible currency, CCP would be shut down almost immediately for.

Then if you want to be a stockbroker wannabe like me, if you want to try your hand at day…I mean…station trading to make that sweet ISK, there is nothing like the thrill of playing the 0.01 ISK war game, and if you are a whale of a size that has the money and the order depth, or the chutzpah of a whale, there is always market manipulation for driving markets wild. Even hardcore and grizzled PvPers are also inherently playing the 0.01 ISK war because ships need to be replaced, and that runs through the mineral markets, which run on tight margins, and are subject to market speculation. Scarce minerals mean scarce ships means scarce battles.

That is key to EVE’s depth, requiring all players to care about the economics, which rewards engagement with the game and the game’s mechanics, and that can drive a game for 23 years.

Data In, ISK Out

Perhaps what makes EVE unique is that CCP publishes an API, with all the data freely available to players. This has not only allowed for an expansive third-party tool ecosystem, but for industrialists and station traders, this is key to building out an empire. In other words, how does a game that is infamously known as “Spreadsheets in Space”, with an official Excel add-on that was built by a Microsoft team, operate without data?

This is what really made the game stick for me. This gave me a reason to try manufacturing and station trading, and after finding Adam4Eve’s API the game became much more sticky for me to stay around. Not only am I learning and practicing my coding skills, but I am also feeling like an important part of the game that I enjoy. PvP is not my favorite part of the game, but if I use my analytical skills and boost my programming skills, all the better, and it helps other players make better decisions on their market moves, that’s golden.

It also makes the immersion better because, despite being on the outside of the game, I can still “play” the game while I am not connected to the game client. The best and longest-lasting games know that if there is no user community “playing” the game outside of the program, the community cannot really form and allow for emergent gameplay inside.

The Visible Hand of the Market

The one thing that keeps the market from going totally off the rails is CCP visibly managing the market when the market is going to cause gameplay issues. Look at the case of my posts on pyerite and asteroid mining, CCP was forced to reckon with the fact if they didn’t fix pyerite’s price, it would have caused issues that would have led to an exodus of players of all stripes. This is also where having a real-life economist on staff is helpful, but I would argue this is helpful for players like me who have access to this kind of data and can give feedback (however informed or ill-informed as you and I may be).

Like the real-life market, governments often step in and course-correct the markets, so the market doesn’t wreck the day-to-day economy. CCP understands that their game is dependent on a healthy and moving market; any type of stalling will inevitably puncture gameplay and time in the game. Linden Labs/Second Life has a similar problem, but since they are dealing with real-life dollars, they are forced to make sure the economy is functioning by the sheer fact that real-life value is ultimately lost for players. Linden Labs is also stuck because, since the world is entirely user-generated, they cannot pull levers like CCP to keep stable and grow their platform (that is not to say that CCP doesn’t have a growth problem).

CCP does not have a perfect track record, by far, but they do try to get it right. But that also requires trust in the community and the community’s trust in CCP. That is how you can manipulate or change the gameplay without, at least, too much consternation (whether r/reve is actually on board with any of CCP’s decisions is another question). Building this relationship is key in keeping a game alive and changing without, well, losing your playerbase.

Conclusion

While the above may feel very real for me, who admittedly is not 1) a hardcore player and 2) still finding my political and industrial legs in this Mariana Trench of a game. That doesn’t mean I don’t know a thing or two, but my perspective is someone late to the party, yet somehow has been roped into coming back for over 10 years, just struggling to find my niche, and economic gameplay is something that I’ve enjoyed over the past year or so, enough so that I’m developing my blog further.

CCP clearly cares about this game and community. A game does not go 23 years in building a legacy for nothing if it doesn’t have (economic) features like this. Very few games that have survived are not at EVE’s level and condition, despite the constant griping. As much as Blizzard/Microsoft tries to continue developing the game and have a healthy user base, it still feels like World of Warcraft struggles with the same type of obsessive dedication that EVE currently does to this day, and that is no accident.

Apparently, these are going to be weekly and I made a promise to myself that I wouldn’t be locking myself into constant, weekly writing (that and I want to write market briefs, and poetry too), so I will see how long I join in on New Eden Banter, at least, on the blog.

Subscribe for my latest posts with New Eden Banter and my market talk.

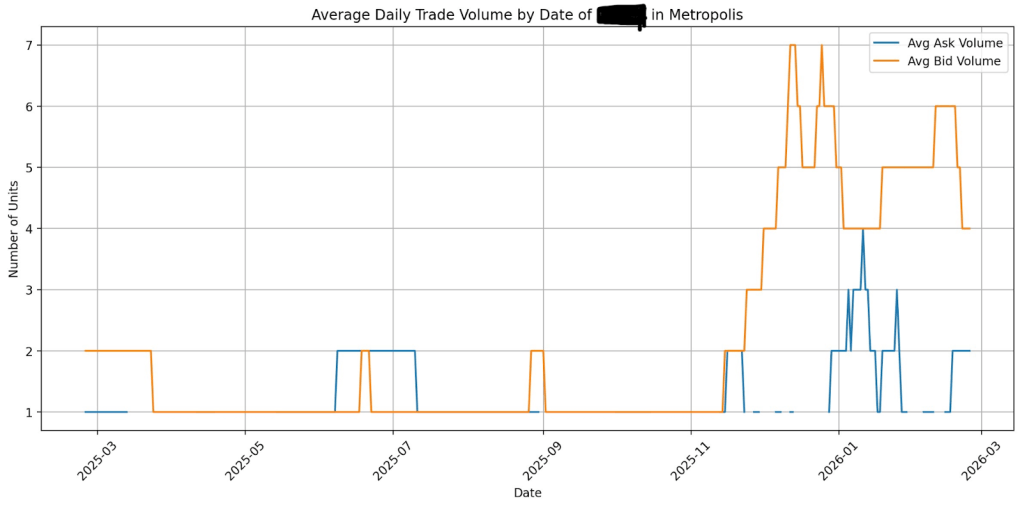

I was discussing the latest meta with a contact on Discord and quickly made some demand curve discoveries that might be signaling things to come in the future of Null Sec politics and territory expansion.

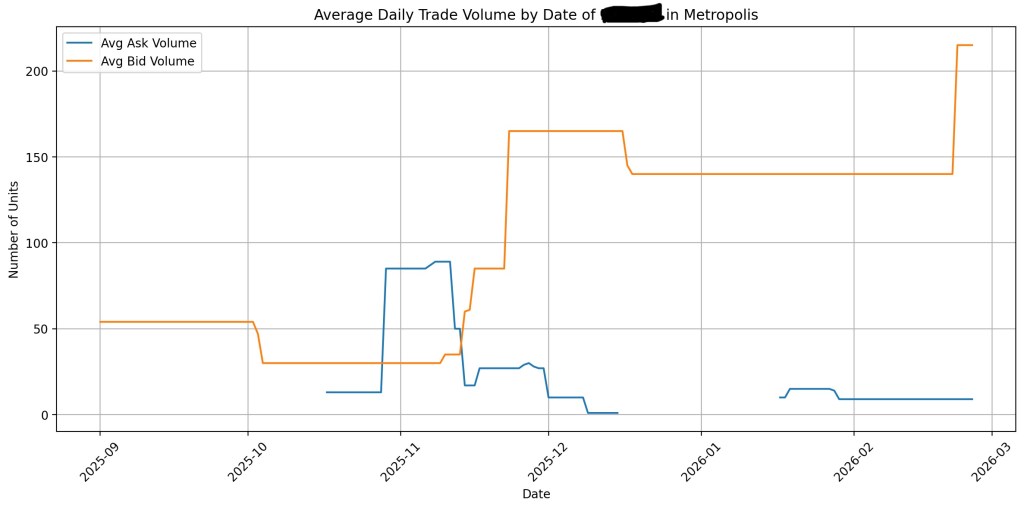

Average Daily Trade Volume by Date of a Carrier-Class Hull in Metropolis from 25/02/25 to 25/02/26Average Daily Trade Volume by Date of a Tech II Light Fighter in Metropolis from 01/09/25 to 25/02/26

Looking into a carrier-class ship, we are seeing greater bid/buy demand outstripping sell/ask volumes in Hek. Additionally, as we look into the current meta for carrier-based fighters, a similar pattern, lined up to the time around the dissolution of PanFam, but also the Carrier buff around the same time, there seems to be evidence of someone in Hek potentially trying to support internal manufacturing with external buys to be on the ready.

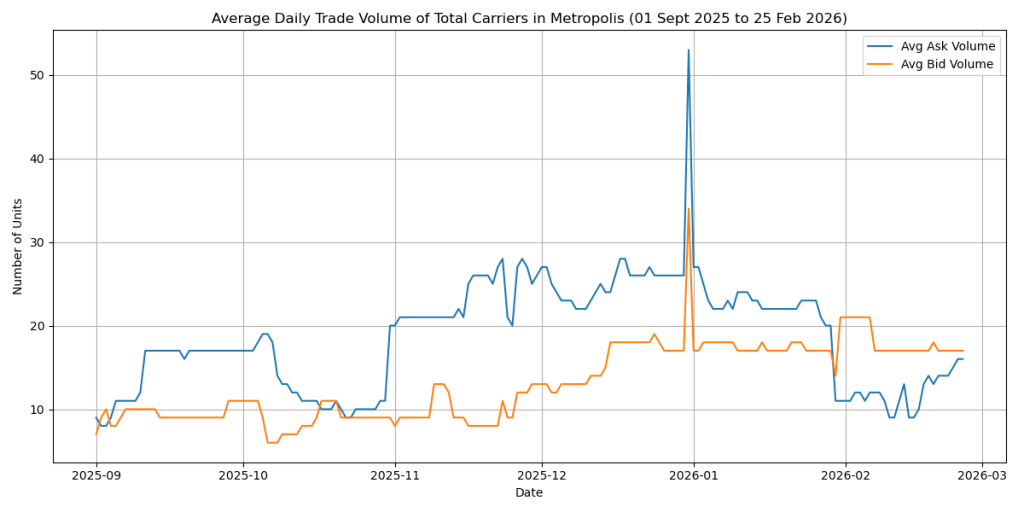

Average Daily Trade Volume by Date of All Carrier Hulls (except Vanguard) in Metropolis from 01/09/25 to 25/02/26

However, broadening the scope to all carriers, this inversion goes away and doesn’t manifest until the end of January of this year. In addition, the big spike in both curves around the end of 2025 suggests that someone was both buying and selling in great quantity. However, given that the spike is on one date and then returns to normal suggests a few things, 1) mistaken orders that were subsequently taken off the market the next day, 2) a data processing issue (the rest of the data looks good and within normal parameters), or 3) vaild short order with the intention to manipulate the market, that was was ultimately resolved the next day.

For null-bloc politics, bringing carrier hulls into hi sec trading hubs is not profitable nor possible (carriers can’t fly in hi sec) given the high-risk nature of bringing high-value cargo into low and high sec space.

If this in fact, a market driven by null sec politics, then null sec is going to start speeding up carrier construction in null sec, considering that there seems to be interest in what is fast becoming the dominant meta. There is potential that this is low sec alliances related, and that given null is quiet at the moment.

The question, of course, on my mind is why Hek? Wouldn’t it be easier to base everything from Jita? It might lie with the fact that Jita and the surrounding area are ripe for ganking squads. Hek is more out of the way in Metropolis and not as directed to as the central location for trade by CCP. Hek is also relatively close to both the Imperium and Winter Coalition null-sec territories. Which side or sides are using Hek as the base of carrier logistic prepping and without any character information attached to order books, we cannot really know. It is clear that someone with a vested interest in the dissolution of PamFam is either rebuilding through hi sec, or prepping for a future escalation.

Hek does have the new advantage of having EVEGuru’s, led by Fern Kitsuen, new industrial park in Anher. There is a good chance that Hek will further develop into the second-largest trade hub. However, given that there are rumors that CCP has plans for developing a more robust trading market, instead of having Jita be the central market, EVEGuru seems to have lucked out.

In other ways, Minmatar space is popular for Faction Warfare content, so it comes with the need for more ships. Carriers can’t roam high sec, Hek would be the primary place to at least stock up on items for FW, so they could be transported. An additional caveat is that my data is looking at region and not system, so while Hek is in Metropolis, and that is useful as a signal, we also run into that limitation, and the carriers being purchased are being traded in low sec.

The main takeaway of this brief basically comes down to if push came to shove and war breaks out, there is likely someone already prepping. If you are a null sec bloc or have vested interests out that way, it is time to start thinking about starting your preparations sooner rather than later. If you are an industrialist, it’s time to start thinking about spreading out and considering other markets that are growing.

I might be back writing (doing a bit of real-life literary writing too), so if you want to catch my market briefs, be sure to subscribe to the blog, when a post goes live. Don’t plan on having a regular day to post, so subscribing is the only way you will see everything

I’m an idiot and said that Nighthawks are Ferox T2, but alas that isn’t true. Post updated.

The big news last week was Legion’s first patch went live on Friday the 9th of this month. The patch devastated entire fleets in seconds without a single shot fired. If the destruction had occurred, the real world value destroyed would have reached the record books.

In short, the rail gun meta was significantly nerfed by the patch, along with a host of many other buffs and nerfs across the empires’ fleet of ships. The patch did more damage than perhaps the Goon/Horde “war.”

The rail gun meta has been popular from the introduction of the Ferox Navy Issue(FNI) in late 2022 until now. Three years of dominance of the hull that now has been undone, providing a more varied approach to fleet doctrines.

Is CCP no fun? Depends on who you ask, but remember EVE pretty much has unlimited ways you can play spaceships, when a meta becomes too locked into fleet composition for too long, the game becomes stale.

Stale gameplay leads to complaints and complaints result in lost subs, and you get the picture.

For today’s post, I am going to look into the FNI after my initial post in June and how the market has changed throughout the months leading up to the patch, and the initial market reaction to the nerf.

Target Scope

Target Market: The Forge

Date Range: 01-05-2025 to 15-09-2025

Commodity: Ferox Navy Issue (FNI)

Observations

As the trend lines show, the hull was generally in decline. Without much destruction, the ask volume increased, depressing the ask price.

Looking at the graph, the FNI’s decline started well before the patch, showing signs of weakness in late June when it was fast becoming obvious that the Goon/Horde war wasn’t going to continue in the same of the initial skirmishes.

On the bid graph things look more volatile, with a one day trough spiking the profit margins (below). While spiky, the profit margin values have stayed relatively stable and flat, though a precipitous fall has happened in the days after the 09-September patch.

In my earlier post in June (highlighted in sky blue), I spotted the inversion of the market, however, despite inverting again, the supply of FNIs outstrips demand.

Going into the final weeks before the patch, supply spikes to the second highest point but as the patch announcement and notes trickle out, FNIs are removed from the market.

Demand sees signs of strengthening, but the reasons why are unclear. I don’t predict for the market to fully recover given the changes in the meta.

Analysis

Is the FNI doomed for all eternity? Depends. Clearly, the current meta of railgun boats is going to change the doctrine make up going forward. Discussing this with corpmates and others online, the Vulture doctrine isn’t going anywhere. While the demand for FNIs will decrease, T1 Feroxes will continue to have use in terms of production of Vulture for fleet warfare.

To be fair to the FNI, while it’s nerfed, I don’t foresee a major crash in usage but it will have less preferential usage and create other opportunities for new ships to enter into fleet doctrines.

Given that FNIs are a separate production line and based on faction dog tags/currency and LP, I imagine demand for both the currency items and the Caldari LP, and therefore prices, will decrease, which will not be significant. The currency items and LP are often used for multiple LP store items.

Industrialists: This is your time to scale back FNI production, and start working with fleet commanders on the next set of doctrine fittings. Continue producing standard T1 Feroxes for T2 production as Vultures, which are still in use in their related game content. The FNI isn’t disappearing, rather its ubiquity is going to decrease. If you are building a large number of these you best bet is to reduce the amount you’re producing and invest production in a more diversified manner.

Station Traders: Hold any further investments into FNI until fleet doctrines start to solidify. I can’t say where to put your bets, as a dominant fleet doctrine has yet to shake out. FNIs are not going anywhere, but going forward fleets will be more varied, which for the long term health of your portfolio, start diversifying now will starve off any problems.

Overall, the markets are shifting due to the recent nerf by the patch on 09-Sept 25 and its effects on fleet composition. The markets should be able absorb this shift and I don’t foresee a crash unless another hull becomes dominant in the fleet doctrine. While change can be difficult in ship doctrine, for both the long term health of the game and the economy it is necessary.

Enjoy my analyses? Subscribe below to get my posts directly to your inbox.

This post is a week late because my boyfriend was in town last week and I chose to spend time with him. Real life always comes first.

Eve is known for its high octane, hardcore PvP culture, though more in terms of blowing up ships and ganking. Given this is a market blog, we are focused on Market PvP everyday. Today, I’m going to discuss the T2 Salvage Market, which is undergoing a pronounced shift given the recent changes in exploration.

Target Scope

Target market: The Forge

Date range: 03/07/25 – 03/09/25

Commodities:

Impetus Console

Power Conduit

Thruster Console

Single-Crystal Superalloy I-Beam

All chosen off of TheOz.Space’s The Week’s OZ Report Dashboard, under priced list for the week of September 1st.

The Data

I start off with the ask and buys of all four components and the trend is down across the board.

There are plenty of spikes and valleys but not ones that are producing strong outliers. As you can see there has been a general decrease from the start of July before the 11 July exploration patch. The rate drop differs after the date, so to apply a blanket statement on the rebalance effect, other than salvage was already going down isn’t the story here.

Spread percentages are rocky but steady but in looking at the Thruster Console, it rose 150% points from 11 July to 03 September, which was beginning of a three day dip in the component that wasn’t experienced by any other of the components studied. The most volatile component was the Single-Crystal Superalloy I-Beam with some bigger spikes but for the most part, the salvage profitability remained stable.

I went in for a deeper dive into the volume for the Thrusters Console to see if I could pinpoint what exactly happened during that initial crash on 11th.

The crash in spread was not due to a supply and demand shift, but rather the shock of the market. However, given that the shock was only evident in the Thruster Console, that should highlight the importance of the material.

Additionally, I know of at least one whale that is heavily influencing the demand in the salvage market resulting in these waves of demand that has pushed the baseline higher.

Analysis

With the Thruster Consoles being prime materials in velocity rigs, the need for them is one of constant demand. For the markets, demand is currently high, whether this actual demand for production demand versus speculators in the market is quite another thing.

Salvage is known for intense speculation. Sir SmashAlot is well known in the EVE station trading community, who is regularly featured on Twitch streamer and market commentator Oz, for being a trillion ISK salvage speculator. Clearly some of the demand above is related to Sir SmashAlot getting into the market at a time when the spread percentage crashed, thus making it much easier to increase demand and move the needle in terms of baseline demand.

It should also be noted that, demand has not consistently outstripped supply, which suggests that the whales are biding their time to collect and then dump at the right time or at least release in spurts to not overwhelm the market.

Given the market is flush and healthy and so is production, there should be no problems with salvage prices becoming volatile overall. While supply is getting further buffed, this will depressed prices, at least for the moment, so again whales are building a stockpile.

This generally means we are going to see hull prices continue to sink and may offset some of the pyerite costs.

Recommendations

Explorers: Amass your salvage and hold onto these items until they are worth more. I would prioritize data sites over relic sites because the data market is still solid, but given the exploration changes affect both types of exploration sites, it is likely data salvage is also likely getting depressed as well.

Station Traders: This is a buy and hold situation. I don’t see spread really opening up until the prices stabilize and CCP finding equilibrium in the salvage markets vs production.

At the end of the day, it’s a lot of whales moving the markets but I would argue to hold onto your salvage until there’s better stabilization of the drop rates and production rates really ramp up.

Enjoy my analyses? Subscribe below to get my posts directly to your inbox.

Pyerite seems to be the consistent story from week to week this month, and the elephant in the room when online with my corp. In the past couple of months, I have been considering creating a mineral index because of its centralness to industry, and because for the past two weeks, all I have thought about is pyerite, industry, and markets, leaving less time for other things to enjoy.

In the resulting discussions from last week’s post on July’s MER, someone chimed in with the fact that other sources of pyerite are going unbuffed by CCP, both R4 moon ore and Gneiss.

The problem with R4 moon mining is unprofitable in comparison to Metenox moon mining, with R4 moons losing their luster as other moon goo becomes more popular with miners, industrialists, and market players. The problem with that is, well, people are leaving pyerite trapped in the moon and not trading in Jita.

Secondly, while low sec enjoys some of the best fights in the game, the mining deposits are a shadow of its High and Null secs brethren, meaning that gneiss is only available for mining in sectors that aren’t conducive to bringing out a big mining fleet. At least with Null Sec, the idea is that the alliances out there are often running their own fleets in the safety of their bloc.

As one can see from these graphs, there isn’t much in the way of gneiss making large profits. While these aren’t demand graphs, clearly the lack of bid activity signals that, at least Iridescent Gneiss, is not in hot demand from buyers.

It is important to note that while the spread percentage of Iridescent Gneiss has skyrocketed in the past month, it may not last. Given that all three types shown here do seem to be on the rise, with the ask price, along with a weakening bid price, the margins seem to suggest that the market has two ways it can go, and it is in a standoff.

Running the volume numbers on Prismatic Gneiss suggests that there is significant demand; however, it is the ask market controls the profit margins. This sets up a price tension that one side is going to have to cave on. Given that the ask volume is trending down, the bid market is clearly meeting the sellers at the ask price, thus boosting the profit margin. Then this drops demand by extension, but also creates a problem with buyers snapping up all the available ore on the market, creating some issues in the long run with supply.

These graphs show CCP is not incentivizing low sec miners to get out to the belts. Given that just regular Gneiss reduces to 2000 units of pyerite, if Gneiss spawn rates were higher, there would be more to effectively reduce down into pyerite, to help the market recover. But there would also be a need to help manage belt security, which CCP will largely leave the miners to the mercy of gankers.

While there is some safety in numbers, mining vessels aren’t all that speedy to warp out and so that could cause more problems. There goes your 1B ISK ship along with all that ore. Mining fleets could ultimately do easy freelance security jobs, getting newbros into low sec and into pvp, but that also could present a mismatch of skill between the gankers outfitted in strong fits and pvp skills and newbros with fits that are going to ultimately be underpowered by lack of pvp skill and experience.

Again, I think at some level that since High Sec mining is the second highest, I do think the high sec buffs are more about helping newbros get into the game and build some ISK wealth so they can ultimately go long term with the game. However, newbros can only do so much mining, especially when the high sec asteroids don’t bring in a lot of pyerite and minerals anyway. Clearly, that is not enough to meet the demand of pyerite and lower the price and sending them out to low sec without proper protection only to get ganked is only dissuading them from continuing.

The sudden influx of pyerite would have the market go haywire, which is probably the reason why CCP is ultimately being highly, and perhaps, overly cautious about pushing moon goo and gneiss too far, but the problem is they still think the price is too high.

The likely story is that most of the pyerite being mined is now being sent through the private contract markets, which is causing the inability to move the price in Jita. At some point, that pyerite does need to come back to the Jita market to affect the price.

Ultimately, the larger problem is CCP looking at the wrong signals on pyerite and ore demand and in order for them to fix the market in the way they see fit they need to be making investments in low sec as a starting point.

Enjoy my analyses? Subscribe below to get my posts directly to your inbox.

Welcome back to Auric Quanta Strategies’ Market Analysis blog. I have been away in real life enjoying my summer and ready to head into the fall strong. I am going to ease back into posting and only post on Thursday for the next few weeks and we will see how the rest of my schedule in real life, corp and business life, and FFXIV all mingle, because somehow I have to keep moving mountains while getting enough sleep.

The July Monthly Economic Report came out this Monday, the 18th of August, which is very late. Supposedly, CCP had issues with their data processing, which seems odd to me that they have such issues given the vast amounts of data they produce with ESI.

The hot topic on everyone’s mind is the status of Pyerite. CCP buffed the output of Pyerite by 10% from Scordites and Morduniums on the 31st, after buffing it in late June.

Pyerite is a foundational mineral in T1 hulls and modules, though T2 hulls and modules are not as constrained by the lack of pyerite on the public markets. So without pyerite, industry begins to halt and there in lies the problem. No ships and modules to build, it becomes more expensive to fly.

Other minerals continue to push the Mineral Price Index down, but the price of Pyerite remains fixed at around 30 ISK, which CCP has deemed too high of cost.

This calculus is informed by the fact that production, both primary (reactions, ore reprocessing, PI, the like) and secondary (modules and hulls), is down in terms of their price indexes and very dramatic fall in terms of production value. However this indicates that the markets have not lost a lot of value, and thus production remains to be viable in the market.

But what does this mean for pyerite and CCP’s push to drive down prices?

Effectively, CCP is trying to push commodities and finished products’ prices lower to effectively make it cheaper and easier to fly, which means more ISK flow and, potentially, more PLEX purchases and redemption.

However, given the multiple buffs of pyerite, supply and demand have not fully reconciled. Looking at the graphs below, there is an uptick in mining value and there is an upswing in asteroid mining volume in null sec after a significant decrease in June suggesting that the alliance shuffle and moves have completed and mining resumes at rates more in-line with numbers from March.

However, key in this is that null sec mining is up, not high sec, and given that asteroid ore that melts into pyerite is not very common in null, means CCP’s attempts to get miners out on the belts will have limited success, at least outside of high sec.

That may be strategic on CCP’s part to get new players a piece of the action they need to get going into solidifying their engagement. The moneyed oldbies and industrial titans need to realize they cannot sustain EVE’s business model indefinitely and that investors in Pearl Abyss cannot wait much longer for EVE to remain a niche of a niche world. That’s the unfortunate reality of late stage capitalism.

Additionally, the MER does not take into account private contracts and corp/alliance buybacks, so it might be making pyerite from CCP’s point of view scarcer than it really is on the ground. This then would explain why the Mineral Price Index and production price indexes are not falling at an even pace. This again suggests that CCP wants newbros actively producing and often times don’t have a strong corp presence.

Takeaways

Miners – Get out on the belts and pop those R4 moons. This is prime opportunity time to get lots of ore in high sec. Low sec also needs mining activity but considering low sec is as, if not more, dangerous than null and sov null these days, do take a few big guns out with you. Low sec has more Mordunium, which reduces into purely pyerite, so if you don’t have access to R4 moons, this is a prime reason to be out in low sec.

Industrialists – No big takeaways other than continuing to produce at the rates you are at right now. If you are short on pyerite and don’t have access to cheap pyerite and/or don’t feel like dealing with the public markets, shift your lines to less intensive pyerite blueprints and focus on salvage now that has effectively lost value on the market given the recent changes in exploration.

Newbros – It’s your time to shine. Get those Ventures mining Scordite, but also fire up the manufacturing modules and get producing. To be super successful takes time, but give it a go and see how it feels!

In short, we will have to sit tight and see how the recent buff on pyerite is ultimately consumed in production in August but we won’t know until the August MER report is released next month.

Enjoy my analyses? Subscribe below to get my posts directly to your inbox.

Before I drop the Auric Intel Report preview later this week, here’s a snapshot of the Vulture market:

📉 Ask prices down 30% (28 May – 15 June)

📉 Bid prices down 22% (28 May – 15 June)

We’re seeing fast-moving price action and likely early signals of a doctrine shake-up or at least a signal the Horde is uninterested in the Goons. Stay sharp.

🗓 Friday: Report preview and goes live

📦 Later this month: Full Vulture doctrine breakdown

→ Make sure you’re subscribed so you don’t miss the drop.